Bussiness

Missed Nvidia? 2 GPU stocks to buy right now

Nvidia (NASDAQ: NVDA) has long dominated the high-end gaming GPU market, with gamers willing to pay premium prices for top-tier performance. However, its 215% growth over the past year raises concerns about the sustainability of further gains, making alternative GPU stocks more attractive for investors seeking robust returns.

GPU companies design semiconductor chips with numerous cores capable of handling complex computational workloads. These chips are crucial in personal computers, smartphones, gaming consoles, and any device displaying images.

Recently, GPUs have expanded their applications beyond graphics. In data centers, GPUs accelerate tasks such as scientific simulations, data analytics, Artificial intelligence (AI) training, and AI inference.

While gaming remains a significant growth driver, AI presents an even greater opportunity. Advanced models like OpenAI’s ChatGPT require immense computing power, necessitating clusters of powerful GPUs.

Cloud computing providers are acquiring GPUs to offer AI services, with Microsoft (NASDAQ: MSFT) projecting its AI cloud services revenue to reach $10 billion. As the demand for powerful computational resources continues to rise, diversifying investments in GPU stocks could offer substantial long-term benefits.

Choosing alternative investments can be challenging. This prompted Finbold to analyze the current market conditions and growth outlooks of various GPU stocks to identify those that are a good buy for the long term.

Intel Corp (NASDAQ: INTC) stock

Intel Corporation (NASDAQ: INTC) is currently trading at $30.97, reflecting a significant decline of 38% since the beginning of the year. Despite facing challenges such as lost market share in CPUs and an economic downturn in 2022, Intel is showing signs of a turnaround.

The company has recently shifted its focus towards AI and manufacturing, hinting at a recovery. Intel’s Gaudi 3 accelerator chips, priced at $15,650, offer competitive price-to-performance against Nvidia’s H100 chips, which cost around $30,000. This competitive pricing could attract significant market share in the burgeoning AI industry.

Moreover, Intel’s focus on expanding its manufacturing capacity, with significant investments and support from prominent investors and the U.S. government’s CHIPs Act, strengthens its future outlook.

The semiconductor foundry market is projected to more than double from $107 billion in 2022 to $232 billion by 2032, and Intel is positioning itself to capitalize on this growth. The company’s strategic shift to a foundry model could make it a leading AI chip manufacturer, especially as it opens new chip plants in the U.S. and abroad.

Intel’s valuation metrics provide encouraging signs for long-term investors. The PEG ratio of 0.43 indicates that the stock might be undervalued relative to its growth potential. Notably, the trailing P/E ratio of 32.26, higher than the forward P/E ratio of 23.93, suggests market expectations of a short-term earnings decline followed by sustained long-term growth.

This dynamic could be driven by Intel’s strategic shifts and recent challenges. Additionally, Intel offers a reliable income stream with a dividend yield of 1.61%.

These factors, combined with its current low trading price and a renewed focus on AI and manufacturing, make Intel an attractive proposition for long-term investors seeking growth potential coupled with a stable dividend income.

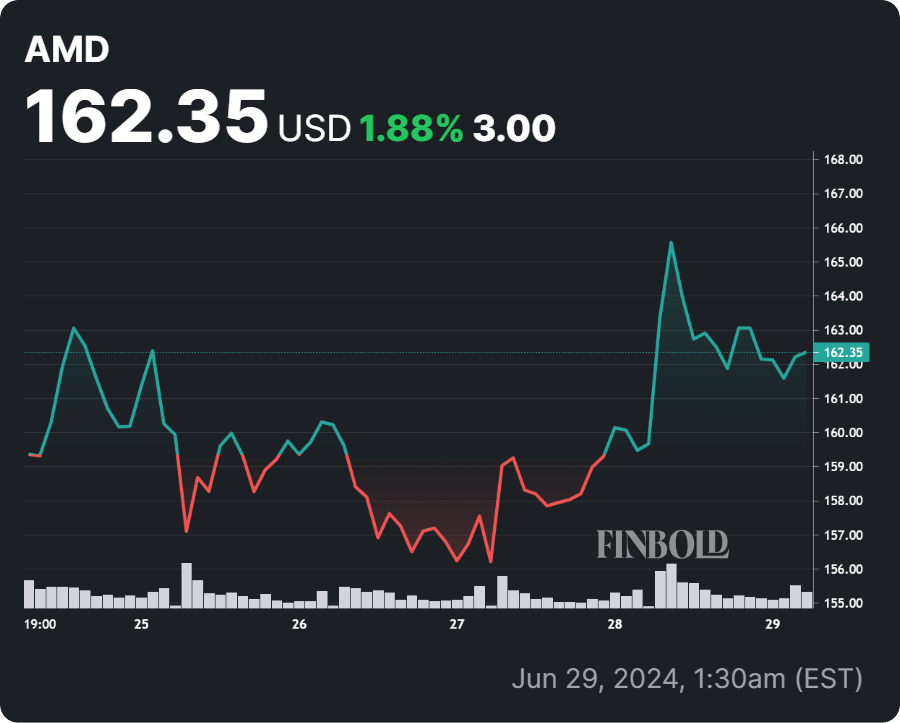

Advanced Micro Devices (NASDAQ: AMD) stock

Advanced Micro Devices (NASDAQ: AMD) is positioning itself as a leading force in the AI sector, garnering a strong buy rating from multiple analysts.

Citi (NYSE: C) forecasts that AMD could secure about 10% of the $15 billion data center GPU market. The company’s growth outlook is reinforced by rising demand for data center infrastructure, with AI chip sales anticipated to hit $4 billion this year, up from a $3.5 billion estimate in January, showcasing the escalating need for AI solutions.

AMD plans to release a new data center GPU annually, beginning with the MI325X and progressing to CDNA 4 architecture in 2025, ensuring ongoing enhancements in AI capabilities. Despite a recent cyberattack by IntelBroker, AMD reported minimal impact on its operations, staying focused on its product development and growth strategy.

AMD’s stock is currently around 30% below its recent peak, which might represent a buying opportunity for those optimistic about the company’s long-term potential amid industry-wide growth.

The company’s valuation metrics are also promising: a market cap of $262.18 billion, an enterprise value of $259.14 billion, and a trailing P/E ratio of 235.09, suggesting significant growth prospects. Furthermore, AMD’s forward P/E ratio of 40.07 reflects positive future earnings expectations.

Its beta of 1.69 indicates higher volatility but also the potential for greater returns. With strong growth potential, a solid product portfolio, and competitive advantages, AMD presents a compelling investment opportunity.

Both of these stocks seem poised for success in the current GPU market, with their potential for growth and strong guidance indicating future gains that could rival or even surpass Nvidia’s.

Nevertheless, investors should exercise caution and perform comprehensive research given the inherent volatility and risks associated with the stock market.

Disclaimer: The content on this site should not be considered investment advice. Investing is speculative. When investing, your capital is at risk

20/7/2024 Horse Racing Tips and Best Bets – Rosehill, Winter Challenge day

"BCCI want Test specialists to play domestic cricket; Rohit, Virat, Bumrah to be exceptions")

BCCI want Test specialists to play domestic cricket; Rohit, Virat, Bumrah to be exceptions

HORSE RACING DAY 5: Andrew Champagne’s picks, analysis, bankroll

HORSE RACING DAY 5: Andrew Champagne’s picks, analysis, bankroll

600 Jobs, 25,000 Seekers: Air India Drive Sets Off Stampede Fear In Mumbai

More Trips, Higher Prices: Business Travel Spending May Finally Top 2019 Levels

Let’s take this offline: why indie fashion boutiques are back in fashion

Blue Jays balance college-heavy Draft with a few high-upside picks

Get to Know Gopher Men’s Basketball’s Frank Mitchell – University of Minnesota Athletics