Family help to get on the property ladder has become the norm in Canada with the size of gifts soaring

Published Jun 27, 2024 • Last updated 3 hours ago • 4 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

The amount of money parents are giving to their children to buy their first home has shot up 73 per cent from 2019 to an average of $115,000. Photo by Getty Images

Article content

Parents giving money to their kids to buy a home took off during the pandemic when real estate went through the roof.

Not really, says a new study by CIBC Capital Markets economists Benjamin Tal and Katherine Judge.

Since 2015, the share of first-time homebuyers who received financial help from family members rose from 20 per cent to 31 per cent, and though that trend has levelled off in recent years, it has not declined.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

“Homebuyers relying on a wealth transfer from their parents in order to purchase a home is becoming the norm in Canada,” said the economists.

Moreover, the amount of these gifts has continued to climb, rising 73 per cent higher than in 2019. The average gift nationally now sits at $115,000.

“While the benchmark home price has fallen by 14 per cent since its COVID-era peak, prices are still 33 per cent above pre-COVID levels, and that means that gifts have risen faster than home prices over that period,” said the study.

Parental support is especially apparent in Ontario and British Columbia, where high home prices have necessitated a higher reliance on family help.

In these provinces, 36 per cent of first-time homebuyers receive a helping hand, five percentage points higher than the national average.

The size of the gifts in British Columbia, Canada’s priciest market, have soared 90 per cent since 2019, well above the national increase of 73 per cent.

Parents here on average are giving their children $204,000 towards a first home.

Even Ontario is tame by comparison. The amount of gifts in this province — where real estate is far from cheap — rose just 52 per cent since 2019 and now sits at $128,000.

Posthaste

Breaking business news, incisive views, must-reads and market signals. Weekdays by 9 a.m.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Posthaste will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

A recent study by Ratehub.ca on how much income is required to buy a home offers clues to why family gifts continue to rise.

Affordability worsened in 11 of the 13 cities the study covers between April and May as homebuyers faced higher mortgage rates and rising home prices in most cities.

In just one month, the income needed to buy a home in Victoria, B.C., rose $1,230 to $172,180 a year.

Vancouver’s required income hit $232,950, up $800.

Hamilton, Ont., saw the biggest increase, Homebuyers now need an income of $171,100 to afford a home here, up $1,550.

Toronto was the exception. The average home price here fell $5,900 between April and May, meaning that homebuyers required $1,250 less annual income.

But the $215,920 a year you need to afford a home in Canada’s biggest city is still out of reach for many.

Wherein lies the problem. Not everybody’s parents can afford to help their children onto Canada’s very expensive property ladder.

Tal and Judge point out that while the phenomenon of parental gifts is helping to ease the bite of housing inflation, it is also widening “the already wide wealth gap in Canada.”

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Sign up here to get Posthaste delivered straight to your inbox.

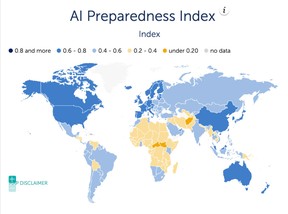

IMF

The International Monetary Fund estimates artificial intelligence could endanger 33 per cent of jobs in advanced economies, 24 per cent in emerging economies and 18 per cent in low-income countries. At the same time it has “enormous potential” to boost productivity, create new jobs and even new industries.

Some countries, however, are more ready for the AI revolution than others. This IMF chart ranks that readiness assessing digital infrastructure, human capital and labour market policies, innovation and economic integration and regulation. Countries in the deeper shade of blue are the most prepared. The United States, for example, achieves one of the highest scores at 0.77, while Canada scores 0.71. Denmark tops the world at 0.78.

CNN hosts the first United States presidential debate, between President Joe Biden and former President Donald Trump, starting at 9 p.m. ET.

Alberta’s finance minister will release the province’s 2023-24 fiscal year-end results.

Today’s Data: United States GDP, personal consumption, durable goods orders and pending home sales

Earnings: McCormick & Co Inc, Walgreens Boots Alliance Inc, Nike Inc.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

The $1 rule, loud budgeting and reverse budgeting: Kelley Keehn, founder of Money Wise Workplaces, knows all the latest trends in personal finance. Watch her video to get tips on how to keep your budget on track during what can be an expensive time of the year.

Are you worried about having enough for retirement? Do you need to adjust your portfolio? Are you wondering how to make ends meet? Drop us a line with your contact info and the gist of your problem and we’ll try to find some experts to help you out, while writing a Family Finance story about it (we’ll keep your name out of it, of course). If you have a simpler question, the crack team at FP Answers, led by Julie Cazzin, can give it a shot.

McLister on mortgages

Want to learn more about mortgages? Mortgage strategist Robert McLister’s Financial Post column can help navigate the complex sector, from the latest trends to financing opportunities you won’t want to miss. Plus check his mortgage rate page for Canada’s lowest national mortgage rates, updated daily.

Today’s Posthaste was written by Pamela Heaven, with additional reporting from Financial Post staff, The Canadian Press and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at posthaste@postmedia.com.

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here.

"BCCI want Test specialists to play domestic cricket; Rohit, Virat, Bumrah to be exceptions")